Introduction

Barrier films are specialized multilayer materials designed to prevent the transmission of moisture, oxygen, light, and other environmental factors, thereby preserving product integrity and extending shelf life. These films are widely used in food and beverage packaging, pharmaceuticals, electronics, and agriculture, where protection against external contaminants is critical.

In the Middle East and Africa (MEA), the barrier films market is gaining momentum due to urbanization, rising demand for packaged goods, and the expansion of pharmaceutical and agricultural sectors. The region’s growing focus on sustainability and circular economy principles is also driving innovation in recyclable and bio-based barrier film technologies.

The Evolution

Barrier films in MEA have evolved from basic polyethylene sheets to advanced multilayer composites incorporating materials like polyethylene terephthalate (PET), polypropylene (PP), polyamides (PA), and ethylene vinyl alcohol (EVOH). These materials offer superior mechanical strength, thermal resistance, and barrier performance.

Initially used in food packaging to prevent spoilage, barrier films are now engineered for specific applications, including pharmaceutical blister packs, electronic component protection, and agricultural mulch films. The development of metalized and transparent barrier films has enabled manufacturers to balance aesthetic appeal with functional performance, while white barrier films are used for light-sensitive products.

Recent innovations include mono-material barrier films that simplify recycling, biodegradable coatings, and smart films capable of responding to environmental changes. These advancements reflect the region’s growing commitment to sustainable packaging solutions.

Market Trends

The MEA barrier films market is shaped by several key trends:

- Sustainability Shift: Manufacturers are increasingly adopting recyclable and bio-based materials to meet environmental regulations and consumer expectations.

- Extended Shelf Life Demand: The rise in ready-to-eat meals, processed foods, and pharmaceuticals is fueling demand for high-barrier packaging that ensures product safety and longevity.

- E-commerce Growth: Online grocery and pharmaceutical delivery services are driving the need for durable, lightweight, and protective packaging.

- Material Innovation: Companies are investing in PCR-grade films, mono-material laminates, and barrier coatings that enhance recyclability without compromising performance.

- Regulatory Pressure: Governments across MEA are implementing plastic waste reduction policies, prompting a shift toward eco-friendly packaging alternatives.

Challenges

Despite its growth, the market faces several challenges:

- Complex Recycling: Multilayer barrier films often combine incompatible polymers, making them difficult to recycle with current infrastructure.

- High Production Costs: Advanced barrier films require specialized machinery and raw materials, limiting adoption among small and medium enterprises.

- Limited Awareness: In some MEA countries, low consumer and industry awareness of barrier film benefits hinders market penetration.

- Regulatory Fragmentation: Varying standards across countries complicate compliance and product standardization.

- Supply Chain Disruptions: Fluctuations in raw material availability and geopolitical factors can affect production and distribution timelines.

Market Scope

Barrier films in MEA are used across diverse sectors:

- Food and Beverage: Packaging for snacks, dairy, meats, and beverages requiring moisture and oxygen protection.

- Pharmaceuticals: Blister packs, sachets, and pouches designed to preserve drug efficacy and stability.

- Electronics: Protective films for semiconductors, batteries, and sensitive components.

- Agriculture: Mulch films, greenhouse liners, and moisture barriers for crop protection and soil management.

- Personal Care: Packaging for cosmetics and hygiene products requiring light and vapor resistance.

Countries such as Saudi Arabia, UAE, South Africa, and Nigeria are leading the regional adoption, supported by infrastructure development, industrial expansion, and government investment in packaging innovation.

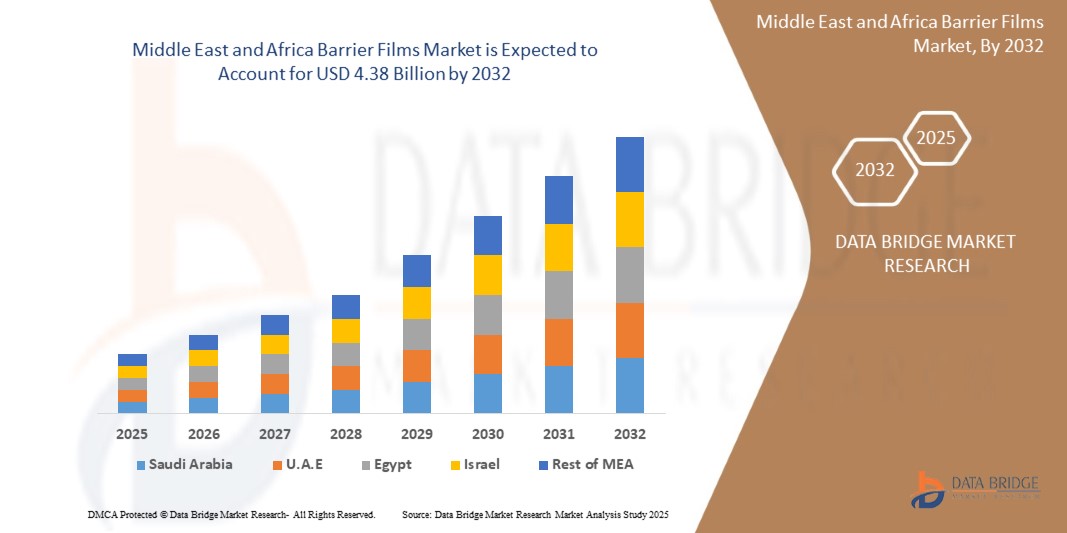

Market Size

The MEA barrier films market was valued at approximately USD 3.23 billion in 2024 and is projected to reach USD 4.38 billion by 2032, growing at a CAGR of 3.9%. Growth is driven by:

- Rising demand for extended shelf-life packaging in food and pharmaceuticals.

- Expansion of urban retail and e-commerce platforms.

- Increased investment in sustainable packaging technologies.

- Adoption of metalized barrier films, which account for over 35% of market share, due to their superior oxygen and humidity resistance.

Factors Driving Growth

Several factors are propelling market expansion:

- Urbanization and Lifestyle Changes: Increased consumption of packaged goods is boosting demand for protective and aesthetic packaging.

- Pharmaceutical Industry Growth: Regulatory requirements for drug safety and shelf stability are driving adoption of high-barrier films.

- Sustainability Goals: The push for recyclable and biodegradable packaging is encouraging innovation in mono-material and compostable barrier films.

- Technological Advancements: Development of smart coatings, multilayer laminates, and nanomaterials is enhancing film performance.

- Government Support: Policies promoting economic diversification and environmental protection are fostering investment in packaging infrastructure and R&D.

Other Trending Reports